Table of Contents

What is buy now, pay later?

Buy now Pay later (BNPL) loans are a sort of installment loan. It divides your purchase into several equal installments, the first of which is due at checkout. The remaining payments are charged to your debit, credit card, or bank account until your purchase is completed.

These plans may include interest and fees, however some do not, depending on the supplier.

When you check out online, you’ll frequently notice BNPL payment plans offered. Providers offer one-time virtual cards for in-store purchases that you may download via the provider’s mobile app, save to your mobile wallet, and spend at the register.

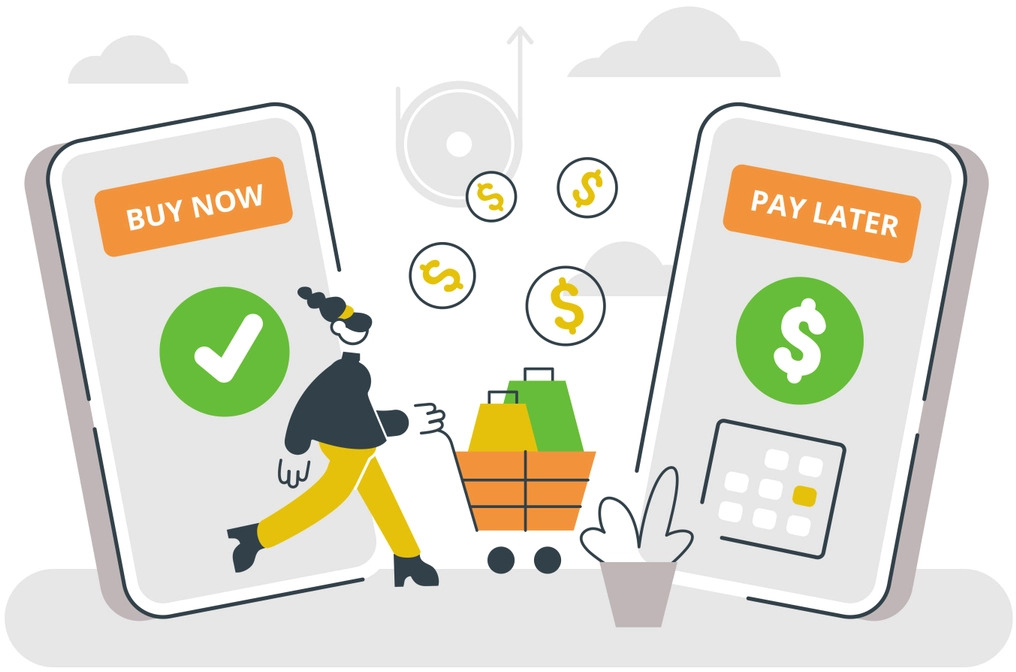

How Buy Now, Pay Later Works

Buy now, pay later (BNPL) programmes differ in terms and conditions, but in general, they offer short-term loans with fixed payments and no interest. You can make the purchase via a BNPL app, or you may have BNPL alternatives through your credit card.

You can use BNPL to make a purchase at a participating retailer and select buy now, pay later at the checkout. If you are authorised, you make a small down payment, such as 25% of the total purchase price. The remaining balance is then paid off in a series of interest-free installments, usually over a few weeks or months.

Payments can be deducted automatically from your bank account, debit card, or credit card. In some situations, you may be able to pay by cheque or bank transfer, while the Consumer Financial Protection Bureau (CFPB) reports that most BNPL lenders provide customers no other option than autopay.

The key difference between using BNPL and a credit card is that credit cards normally charge interest on any balance carried over to the next billing cycle. Although some credit cards offer 0% annual percentage rates (APRs), this may only be for a limited time. With a credit card, you can carry a balance or use your credit line indefinitely.

BNPL apps usually do not charge interest or fees and have a set repayment period. You are aware of your payment amounts in advance, and each payment will be the same.

Risks of Using BNPL Apps

There are several dangers to consider before entering into a BNPL arrangement.

Because BNPL financing is not as tightly regulated as credit cards, you should first comprehend the repayment terms to which you are consenting. Terms can differ greatly. Some organisations, for example, may demand you to pay the remaining debt in biweekly installments over a month. Others may allow you three, six, or even twelve months to pay off your goods.

Finally, look at store return policies and how buy-now-pay-later loans may affect your ability to return something you’ve purchased. For example, a merchant may enable you to return an item, but you may not be able to terminate the buy-now-pay-later agreement until you present documentation that the return was approved and processed.

Pros and Cons of Buy Now, Pay Later

Pros:

- Convenient method of paying for products over time

- Credit cards frequently have no or lower interest rates than debit cards.

- It is not necessary to have good credit or a high credit score to qualify.

- Quick approval

Cons:

- Payments might be difficult to track.

- Late penalties and credit score loss arise from missed or late payments.

- No rewards or cash back earned on purchases

- Payments may continue even if the item is returned.

What apps allow you to buy now and pay later?

- Affirm collaborates with retailers such as Amazon and Walmart. While its pay-in-four plan is always zero interest, its monthly payment plans with periods up to 60 months may charge 0% to 36% APR. Affirm does not incur late fees.

- Afterpay collaborates with shops such as Old Navy and Gap to provide interest-free pay-in-four and monthly plans of six or twelve months. APRs for monthly plans range from 0% to 35.99%. There are no additional costs with Afterpay as long as you pay on time. If your payment is not received within 10 days of the due date, you will be charged a $8 late fee.

- Apple Pay Later can be used anywhere Apple Pay is accepted online or in-app. Apple’s pay-in-four plan has no interest and no fees. Users must link their Apple Pay Later subscription to a debit card, and payments are managed using the Wallet app.

- Klarna is available in places such as Sephora and Macy’s. Klarna’s pay-in-four plan does not incur interest, but if you are more than 10 days late on a payment, you will be charged a late fee of up to $7. Klarna also provides monthly payment plans ranging from six to twenty-four months with APRs ranging from 0% to 29.99%.

- PayPal has a pay-in-four and monthly payment plan available online and through its mobile app at retailers such as Best Buy and Home Depot. The pay-in-four option is interest-free, while plans of six, twelve, or twenty-four months vary from 9.99% to 29.99% APR. Late fees are not charged by PayPal.

- Sezzle, which is available at thousands of merchants including Target, charges no interest when paying in four installments. Though it does not charge a late fee, if you miss a payment, your account is deactivated after 48 hours and you must pay a reactivation fee of up to $15 to use Sezzle again. After your initial down payment, Sezzle may charge a fee of up to $5 for using a debit or credit card.

- Zip can be found anyplace. When you download Zip’s mobile app, Visa is accepted. It charges an installment fee if you use its pay-in-four option. This cost ranges from $4 to $6, depending on the amount purchased. It also levies a late fee of $5, $7, or $10 for missing payments, depending on where you live.

Final Thoughts:

Buy-now-pay-later (BNPL) loans allow you to buy purchases right away but pay them off over time with no interest. If you’re thinking about using a BNPL plan, be sure you understand the terms and conditions and that you’ll be able to make all of the payments on time. Consider whether the payments are affordable and what penalties you might face if you can’t make them.